1. Fixed-Interest Home Loan

How It Works:

- Your interest rate will remain the same through the life of the loan

- The payment of the loan is split equally into monthly installments

- Only a small part of your beginning payments will be paying off the principal of the loan, because the interest portion of the payments are front-loaded (meaning you’re paying down more interest first to save yourself some money later)

- You can get a 10, 15, or 20-year loan (and sometimes other variations), but a 30-year fixed loan is the most common option

Who Is A Fixed-Rate Mortgage Loan For?

A fixed-interest loan is one of the most common. It’s good if you want a variety of loan lengths to choose from, and if you like your monthly payments to remain the same to help you budget. It’s also good if you want to be building equity (since you’re paying both principal and interest), and if you want to benefit from the possibility of interest rates rising.

Try this mortgage loan amortization calculator to estimate your monthly loan repayments. It will show you how much of your repayments will go towards the principal and how much will go towards interest.

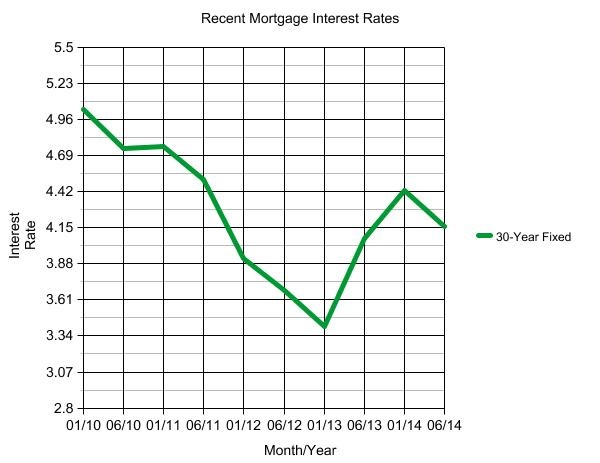

The above image shows how interest rates on 30-year fixed rate mortgages have fluctuated over the past few years. If you want to see rates for your specific state, just choose it from the dropdown box here.

Pros:

- Payments are the same each month

- Predictable payments allow you to keep control of your budget

- If interest rates begin to rise, you’re still paying the same, lower amount you originally got your loan at

Cons:

- Monthly payments are higher than interest-only loans (see the third loan type of this list) because they include payments on both the principal and interest

- If interest rates begin to fall, you’ll still be stuck paying the same interest rate that you agreed upon in the beginning

2. Adjustable-Rate Mortgage (ARM)

How It Works:

- The interest rate can go up and down throughout the life of the loan depending on the market

- This means your monthly payments can fluctuate

- The initial interest rate is typically fixed for a certain period of time, after which it’s adjusted periodically

Who Is An Adjustable-Rate Mortgage For?

If you believe that interest rates are going to fall, you might go with an ARM so you’re not stuck paying a high interest rate at a fixed percent. ARMs also might be good if you know that your income will increase in a few years, so you can have a lower interest rate to start out before your increased income can afford a potentially higher one.

Adjustable-rate mortgages are good if you know you’ll only be in the loan for a few years, since they typically come with a significantly lower interest rate to start. If you know you’re going to move or be able to pay off the loan in a few years time, this type might be for you.

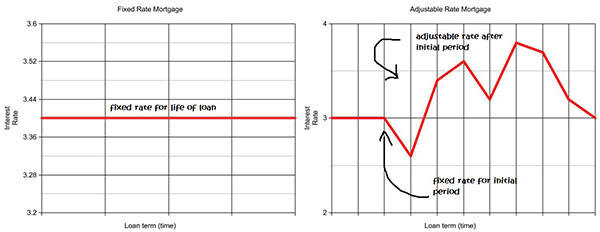

The graphs above show the contrasting behaviors of fixed rate mortgages and adjustable rate mortgages. They’re for illustrative purposes only (no hard data was included).

Pros:

- Interest rate caps are included so a limit is set on how high the interest can go

- The initial interest rate is usually set lower than a typical fixed-rate loan

Cons:

- Since your monthly payments fluctuate after the initial rate period, it can be a challenge to budget around it if your payments increase

- Some ARMs come with a prepayment penalty, which is a fee you can be charged if you sell or refinance the loan

- You might not be able to get as big of a loan

3. Interest-Only Loan

How It Works:

- You only make monthly payments of the interest on the mortgage (and not the principal) for a fixed period

- The interest rates can fluctuate as often as every month or may be fixed for a 10-year period if it’s an ARM

- Because interest-only loans favor the bank, you might be able to qualify for this loan if you can’t qualify for others

Who Is An Interest-Only Loan For?

Interest-only loans might be great for you if you initially want lower monthly payments, but know you’ll be making more money in the future to make increased monthly payments on the loan balance (or even pay it off in a lump sum).

They’re also good if you never intend to fully pay off your mortgage (essentially treating it like renting), such as if you have plans to sell the house in a short period of time or relocate.

Try this simple interest-only loan calculator to get a better idea of what your payments could be.

Pros:

- Since you’re initially only paying interest and not principal, your monthly payments are typically going to be lower they they would on a fixed-interest or ARM loan

- Lower monthly payments allow you to save for other expenses or invest elsewhere

- During the interest-only period, the monthly payment is tax-deductible

Cons:

- The loan balance remains unchanged, unless you pay extra on top of the monthly interest payment (you should if you can)

- When paying off the principal at the end, the payments increase

- If you’re only paying interest, equity is not being built (since you aren’t paying down the principal)

4. Federal Housing Administration (FHA) Loan

How it works:

- These loans allow you to buy a home with a small down payment

- They are Insured by the FHA, which makes a guarantee to your bank that it’ll pay your loan if you can’t

Who Is An FHA Loan For?

FHA loans are great if you don’t have enough money to pay at least 20 percent down on your home–maybe you’re a first-time home buyer, a recent college graduate, or a newlywed.

They’re also good if you have a low credit score, or if you didn’t qualify for a conventional loan. Since there are limits to how much you can borrow, an FHA loan is good for a starter home or a less expensive home.

It’s important to note that sometimes, you can still buy a home with a small down payment using a standard loan (not an FHA loan). It’s definitely possible to find great offers that beat FHA loans, especially if you have good credit, so make sure you shop around for all kinds of loans before you make your final decision.

Pros:

- No income limits

- Can get a loan with as little as 3.5 percent down with a credit score as low as 580

- Can get gifts from the seller to cover all or some of the closing costs

- No prepayment penalty

Cons:

- There’s a debt-to-income ratio to qualify

- There are limits to how much you can borrow–visit the HUD’s site to check the borrowing limits in your area

- The FHA charges an upfront borrower’s fee (mortgage insurance premium, or MIP) or 1.75 percent

- After paying the upfront fee, you must continue to make smaller monthly payments for mortgage insurance and it can end up costing more the private mortgage insurance

- You’ll end up paying more interest than with a conventional loan (since you’re not putting down at least 20 percent)