When it comes to buying a home, negotiating with the seller is the part of the process that fills many first-timers with dread. But the negotiation process doesn’t have to make you break out in a cold sweat. With a few deep breaths and a few good tips, you can bring out your inner Donald Trump and get a great deal.

1. Know What You Can Spend

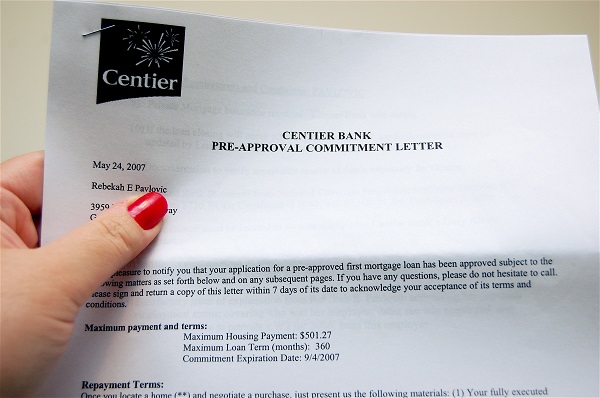

The first step to putting in a winning offer is to get pre-approved. Putting together your financial information for the bank may be a bit of a hassle, but it’s well worth it.

Here’s why:

- Pre-approval lets you know how much you can spend—according to the bank, not you (see #2 below)—so you can make a confident offer.

- It lets the seller know that you’re a serious buyer, which can only make your offer more desirable.

- Some buyers’ agents won’t even submit an offer and some sellers’ agents won’t accept an offer without pre-approval.

2. Know What You Should Spend

The bank may pre-approve you for a certain amount, depending on factors like your income and any already existing debt, but that doesn’t mean you should spend as much as they’re willing to lend you. Only you can decide how much of a financial obligation you’re comfortable with.

Here are some questions to consider while coming up with your magic number:

- If you love to travel (or eat out or shop) and a higher home loan is going to wipe out your annual “extras” budget, will you be happy in the long run?

- Are you planning on taking a financial step back soon, perhaps to start a family or go back to school? The bank may not know about this impending change to your finances, but you do. Make sure you can afford the monthly payments even after this downward financial shift.

- Does the payment still allow you to save money? If every dollar has to go toward your mortgage and other monthly expenses, you’ll have no wiggle room if a big repair comes up down the line.

Keeping in mind what you may be sacrificing to buy a higher-priced home will stop you from rushing to up your offer during negotiations.

3. Know Your Market

In many markets across the country, the housing slump is over and prices are heading back up. In the San Francisco Bay Area, for example, home prices are now higher than they were during the previous peak in 2006.

Buyers in this market, and other hot areas like Seattle and Dallas, are at a distinct disadvantage and sellers know it. When they’re receiving multiple, sometimes all-cash, offers they aren’t going to be very open to concessions.

But in other markets, due to increased inventory, first-time homebuyers can definitely find a deal. The number of homes available in a particular area, the average sales price, and employment trends for the region are all factors that lead to good markets for first-time buyers.

Major metropolitan areas like Pittsburgh, Tampa, and Orlando are all good places to buy right now. For each city-specific listing page, Movoto shows the market statistics for the past few years.

Click here to see the trends for your city.

In a cooler market:

- Go into negotiations with the knowledge that the seller probably needs to sell, otherwise they’d wait for a better market.

- Remember that there are a lot of homes available in the market and, if you don’t get this one, another one will come along!

- The factors that are causing lower sales prices in an area, such as higher unemployment and overproduction of housing, may not be temporary. If you bid too high on a home, it may take many years before you get a return on your investment.

4. Know Value, Not Just List Price

The listing price shouldn’t scare you off of a home, but it shouldn’t get you too excited either. Instead, take a look at the home’s actual value, based on comparable home sales in the area. Then consider the list price and create a successful strategy from there.

If a home is slightly underpriced for the area…

Don’t offer below list price and assume you have room to negotiate up. Someone else may come along and snatch the house away from you. In these cases, your first offer may be the only offer you get to present, so make it a good one.

In certain hot markets, a common tactic is to underprice homes dramatically in order to create interest and, eventually, a bidding war between buyers. If you really want the home, you may need to offer well over the asking price and make other concessions to make the deal.

If a home has been sitting for a while at the same price…

It may be a good opportunity to come in with a lower offer before the sellers drop the price. Negotiating directly with the sellers, who may finally be coming to terms with the fact that house is not worth as much as they thought, will be a lot easier than competing against other buyers after a dramatic price cut.

If the seller drops the price and it’s now more in line with the market…

Don’t wait to make an offer! Just because a home was sitting for months at the higher price doesn’t mean it will keep sitting once the price comes down.

This is an area where a knowledgeable real estate agent can really make the difference. You can search for real estate agents, who are all knowledgeable experts in their local markets.

5. Know It Isn’t Personal

Buying a home can be as much an emotional decision as it is a financial one. When you finally find your dream home, but the seller isn’t willing to accept your final offer—the one you carefully crafted based on your pre-approval amount, the monthly payment you’re comfortable spending, and your knowledge of the market trends and values in the area—it can feel frustrating, even infuriating.

But remember:

- The seller isn’t trying to make you crazy, even though it may seem like it. They simply think the home is worth more than what you’re willing to spend, and they may or may not be right.

- Selling is an emotional decision, too. If you feel attached to a house after touring it a few times, imagine how you’d feel after you’d lived in the home for years, started a family and watched your kids grow up there. The seller may see more value in the home than there really is based on these emotional ties and it’s difficult for even the best real-estate agent to talk them out of it.

- They may end up deciding to reduce the price down the line, but haven’t yet accepted the market realities in the area. If a deal isn’t in the cards this time around, it doesn’t mean it never will be.

You want to end your initial negotiations on good terms, so that if and when the sellers are ready to make a deal, you’re the one they call first.

Emily Landes is a writer and editor who is obsessed with all things real estate. She also has a DIY problem that she blogs about at pritical.com.